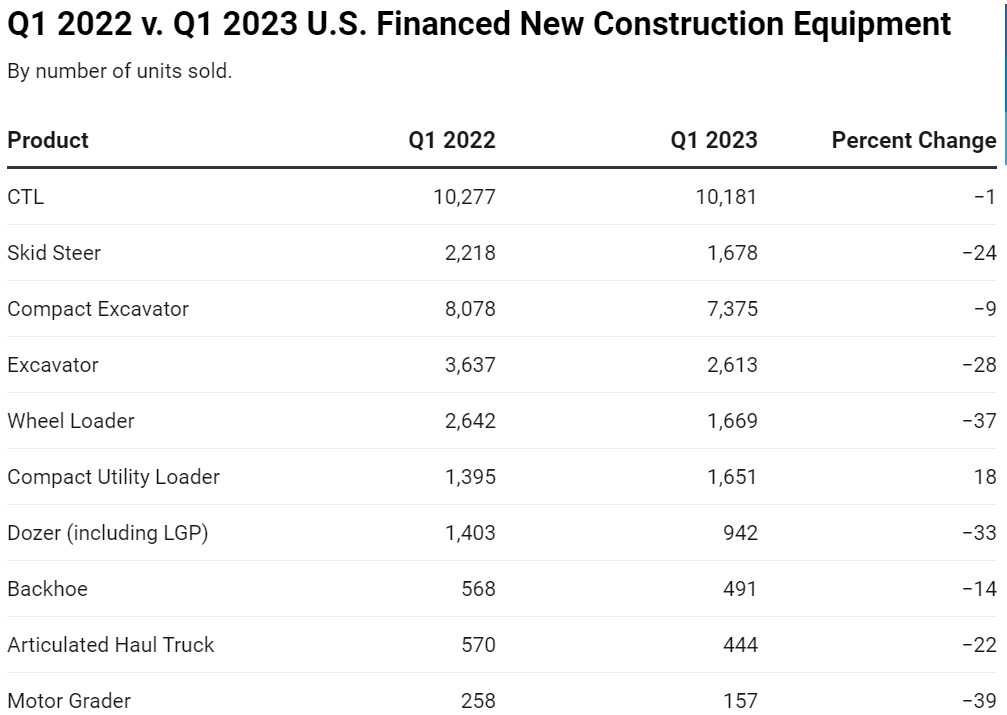

According to EDA’s UCC-1 data, compact utility loaders emerged as the sole highlight in year-over-year Q1 comparisons for financed new equipment sales, experiencing a significant growth of 18.4%.

During the first quarter, two additional categories of compact machines experienced only slight decreases in sales. New compact track loaders witnessed a marginal decline of 1%, while compact excavators saw a modest decrease of 9%.

Among the remaining seven machine types analyzed, all experienced substantial double-digit declines during the quarter. Motor graders were hit hardest with a significant drop of 39%, followed by wheel loaders (-37%), dozers (-33%), excavators (-28%), skid steers (-24%), articulated haul trucks (-22%), and backhoes (-14%).

Compact utility loaders grow

Despite being a low-volume category in general, compact utility loaders continue to display growth, with new entrants continuously joining the market.

During ConExpo 2023, Case CE provided a sneak peek of its inaugural mini track loader, the TL100, while Wacker Neuson expanded its lineup by introducing two additional models, namely the SM60 and SM120.

In the first quarter of 2023, financing was obtained for 1,651 new compact utility loaders, marking an increase from the 1,395 units financed during the same period in 2022. The leading new models in terms of sales were the Bobcat MT100 (427 units), Kubota SCL1000 (163 units), and the Toro Dingo TX1000 (115 units).

Compact track loaders remain on top

In the meantime, compact track loaders maintained their dominant position in terms of sales volume, surpassing all other product categories.

In the quarter, financing was obtained for 10,181 new compact track loaders, indicating a substantial lead over the next highest category, compact excavators. The number of CTLs sold was nearly 40% higher. Among the top-selling new financed CTLs were the Kubota SVL97-2 (1,547 units), Kubota SVL75-2 (1,371 units), and Cat 259D3 (679 units).

Despite the overall dominance of compact track loaders, it is worth noting that in the Northeast and West USA’s regions, more compact excavators were sold during the quarter. In the West, a total of 1,361 compact excavators were financed, surpassing the 1,034 CTLs. Similarly, in the Northeast, 1,039 compact excavators were financed, while 812 CTLs were financed. For a detailed breakdown of the states included in each region, please refer to the Methodology section below.

Kubota continued to dominate the list of best-selling compact excavators, with its KX040-4 (591 units) and KX057-5 (436 units) leading the pack. Deere secured the third position with 411 newly financed units of its 35G model sold.

New financed heavy equipment sales

While compact machines remained the primary focus, we also explored three full-size machine categories, namely excavators, wheel loaders, and dozers (including low ground pressure, or LGP, models). Here are the top models for the quarter in terms of the number of units financed:

Excavators:

- John Deere 85G (99)

- Bobcat E88 (89)

- Komatsu PC210LC-11 (84)

Wheel Loaders:

- John Deere 634P (87)

- Komatsu WA270-8 (86)

- Deere 544P (76)

Dozers:

- John Deere 650K (66)

- John Deere 700L (63)

- John Deere 850L (60)

Brand moves

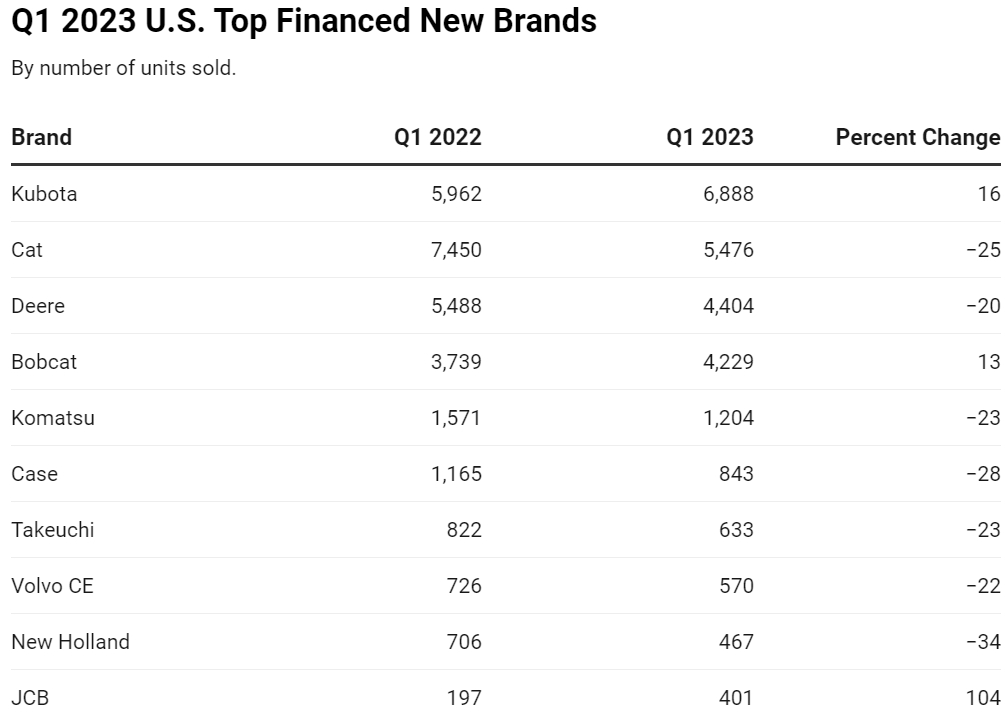

During Q1 2023, three brands experienced growth in the number of units financed compared to the same period last year. The most substantial increase was seen by JCB, with a remarkable surge of 104%. Kubota and Bobcat also achieved double-digit gains, with a 16% and 13% increase, respectively.

New Holland witnessed the largest decline in the number of units financed for the quarter, experiencing a significant drop of 34% from 2022 to 2023. Furthermore, all other brands within the top 10 also encountered double-digit decreases: Case (-28%), Cat (-25%), Komatsu (-23%), Takeuchi (-23%), Volvo (-22%), and Deere (-20%).

Methodology

EDA, a division of Randall Reilly, the parent company of Equipment World, serves as a reliable source for tracking UCC-1 filings. These filings are utilized by lenders during the financing process of machines.

The proportion of financed machines varies depending on the type, ranging from 40% to 75% of the total number of machines sold in the United States. It’s important to note that these figures exclude machines purchased through cash transactions or letter of credit, focusing solely on the financed segment.

EDA reports undergo regular updates, and it is important to note that the numbers presented here, while reflecting the majority of Q1 2023 results, may have undergone slight changes since the data was last pulled in early May.